Archer Daniels Midland (ADM) is a long time Dividend Aristocrat. It has a sustainable business for many decades to come, but history suggests little in the way of growth prospects. The only way an investor can realize a return from an investment in shares is through receipt of dividends and gains on sales of shares. I repeat – the only way. Past performance indicates receipt of dividends is fairly assured for Archer Daniels Midland, along with dividend growth. Normally, I would say there is little in the way of potential share price growth prospects for ADM. That is not the case at present. The current beaten down share price provides an attractive entry point to boost dividend receipts, and maximize the potential for share price gains.

About Archer Daniels Midland

Excerpted from Archer Daniels Midland’s 2018 10-K:

Archer-Daniels-Midland Company (the Company) was incorporated in Delaware in 1923, successor to the Daniels Linseed Co. founded in 1902. The Company is one of the world’s leading producers of food and beverage ingredients, and other products made from a variety of agricultural products. The Company’s products include natural flavors and colors, health and nutrition products, vegetable oil, corn sweeteners, flour, animal feed, and biofuels. The Company has an extensive global grain elevator and transportation network to procure, store, clean, and transport agricultural commodities, such as oilseeds, corn, wheat, milo, oats, and barley, as well as products derived from those inputs. The Company is principally engaged in procuring, transporting, storing, processing, and merchandising agricultural commodities, products, and ingredients. The Company uses its significant global asset base to originate and transport agricultural commodities, connecting to markets in more than 170 countries. The Company also processes corn, oilseeds, and wheat into products for food, animal feed, chemical and energy uses. The Company also engages in the manufacturing, sale, and distribution of specialty products including natural flavor ingredients, flavor systems, natural colors, proteins, emulsifiers, soluble fiber, polyols, hydrocolloids, natural health and nutrition products, and other specialty food and feed ingredients. The Company uses its global asset network, business acumen, and its relationships with suppliers and customers to efficiently connect the harvest to the home thereby generating returns for our shareholders, principally from margins earned on these activities.

Archer Daniels Midland is a cyclical business, involving up and down yearly profits, but with solid long-term results. Share prices tend to fluctuate with yearly profits. Archer-Daniels Midland shares appeared to be close to the top of a cycle recently, with shares breaking above $51.00 briefly in August 2018. Buying shares at the top of a cycle may lead to poor returns on investment. Buying at the bottom of a cycle, at depressed share prices will provide better returns. The current trade wars may be contributing to a temporary fall in Archer Daniels Midland’s share price to around the $42 level. A returns-based investing approach will identify if this represents an attractive entry point, with the share price anticipated to return to higher levels sometime over the next 3 to 4 years.

A Systematic Approach To Reviewing ADM’s Past And Projected Future Performance

What I need to do now is undertake the process of determining whether a purchase of ADM shares at current prevailing prices is likely to provide an acceptable rate of return going forward. This process requires a look at the past, and quantification of a range of future expectations for ADM. TABLE 1 below summarizes a sampling of results from investing in ADM over the last 4 to 5 years and exiting at the current low share price.

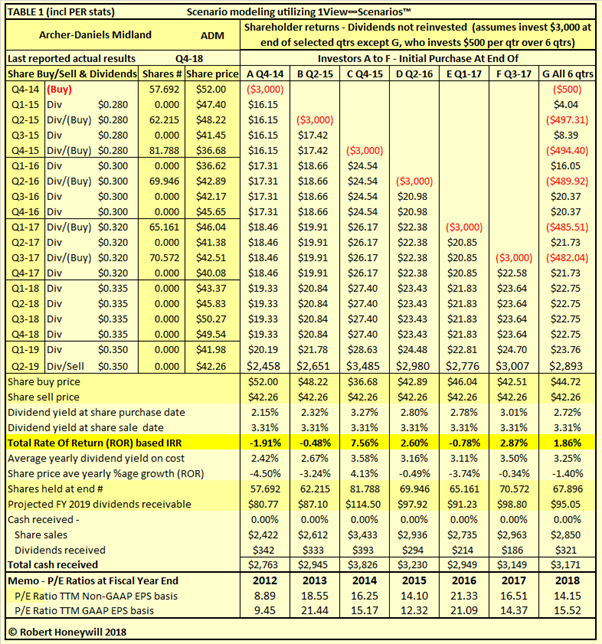

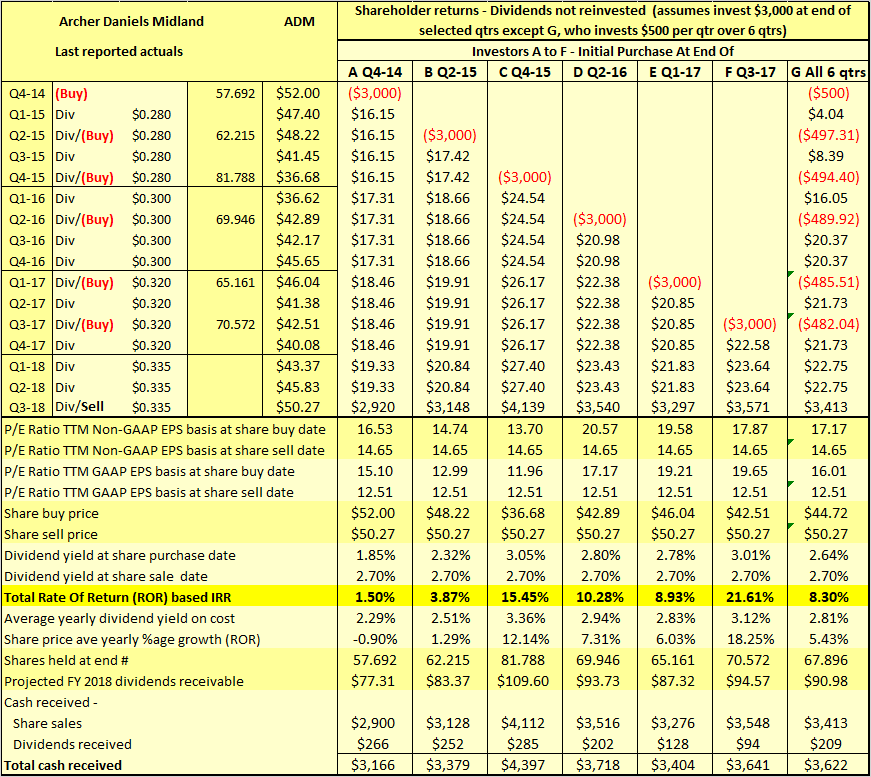

ADM Historical Shareholder Returns

TABLE 1

{kind=link}

Variability in returns presents risk and opportunity

TABLE 1 above shows the results were very different for 7 different investors, each investing $3,000 in ADM over the last 4 years, Average yearly rates of return range from negative 1.91% for investor A, to 7.56% positive for investor C. Such a wide range of returns indicates a degree of volatility and risk. These are not just hypothetical results, they are very real results for anyone who purchased shares on the various dates and held through to April 2, 2019. Of course, if there had been an exit in the second half of 2018, at a share price ~$50 the results would be far more favorable. Where there is risk there is generally opportunity – there for anyone to take advantage of. For a long term, or dividend growth investor, now is not the time to exit an investment in ADM shares. But it may be an opportune time to enter an investment in ADM shares as explained in detail below.

My proprietary dashboards (see further below) allow an investor to project similar data to that contained in TABLE 1 and conduct an infinite amount of scenario testing to see what returns might be available from an investment in ADM shares at today’s price levels. I believe this quantitative approach is far superior to using Betas, forward P/E ratios, PEG ratios and other indicators to qualitatively review the prospects for an investment in shares. I feed analysts forecasts into my dashboards as part of the process of converting available qualitative data into projected rates of return. The nature of this forecast data leads to analysts quarterly consensus forecasts not adding up to analysts full year consensus forecasts. Some moderation is required as shown in TABLE 2 below.

TABLE 2

Where the analysts weighted average consensus forecasts do not add to the equivalent full year EPS, the quarterly EPS is adjusted per the “Adopt” column. The EPS amounts per the “Adopt” column in TABLE 2 above have been used in the Dashboard Base projections further below. In addition, dividend increases have been input at a rate of $0.015 increase to the quarterly rate effective in the first quarter of each year. TABLE 3 below summarizes various historical financial data for ADM for purposes of comparison when assessing the reasonableness of our dashboard projections.

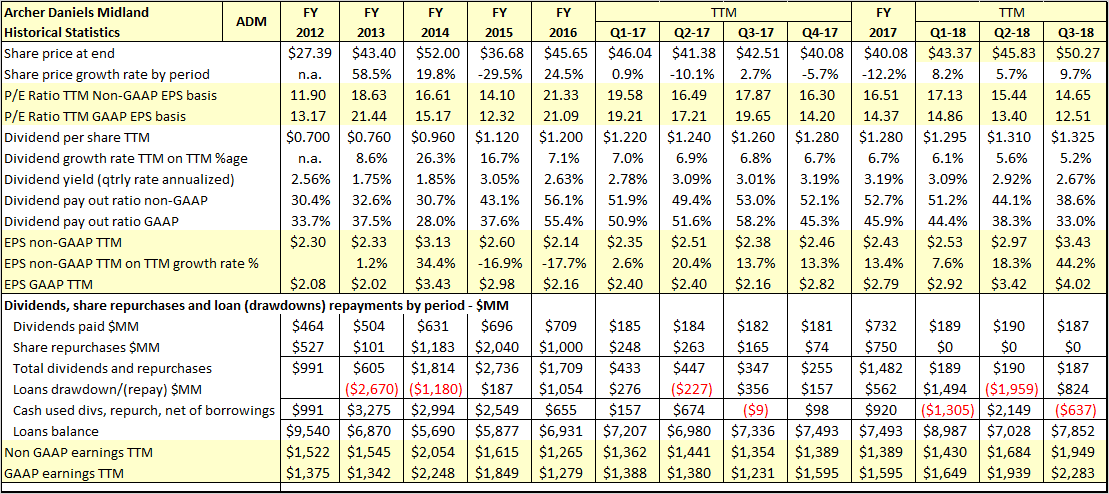

ADM Historical Financial Data Summary FY 2012 to FY 2018

From various data inputs the historical financial data summary per TABLE 3 below is auto-generated.

TABLE 3

{kind=link}

In a forum discussion on forward P/E ratios (note: forum accessible only to SA contributors), author Michael Boyd wrote:

I’d (personally) love non-GAAP numbers on a trailing basis (EBITDA, P/E, etc.). Short of Bloomberg, don’t think many providers are giving that. I’ve got to backtrack and model all that stuff by hand as it stands today. Generally I go back at least three years so that doesn’t necessarily help me, but I think there is a market for that. No use comparing ttm GAAP P/E or EBITDA to forward earnings estimates.

What Boyd wrote made sense to me, so I have made sure to include both GAAP and non-GAAP P/E ratios in both my historical data and in forward estimates. The historical summary for ADM reveals a lack of long-term growth in EPS and share price. But on average, ADM is a steady earner generating excess cash to pay dividends and make share repurchases. Share repurchases over the last 7 years to end of 2018 total $5.601 billion, compared to total dividend payments of $4.488 billion over the same period. Over the same period borrowings were reduced by $1.152 billion from $9.540 billion at end of 2012 to $8.388 billion at end of 2018. Cutting back on share repurchases would allow for increasing dividends at a faster rate and/or paying down debt. We now are in a position to review the auto-generated projected financial summaries. The first of these is our TABLE 4 Base projection dashboard which incorporates the projected data included in our input.

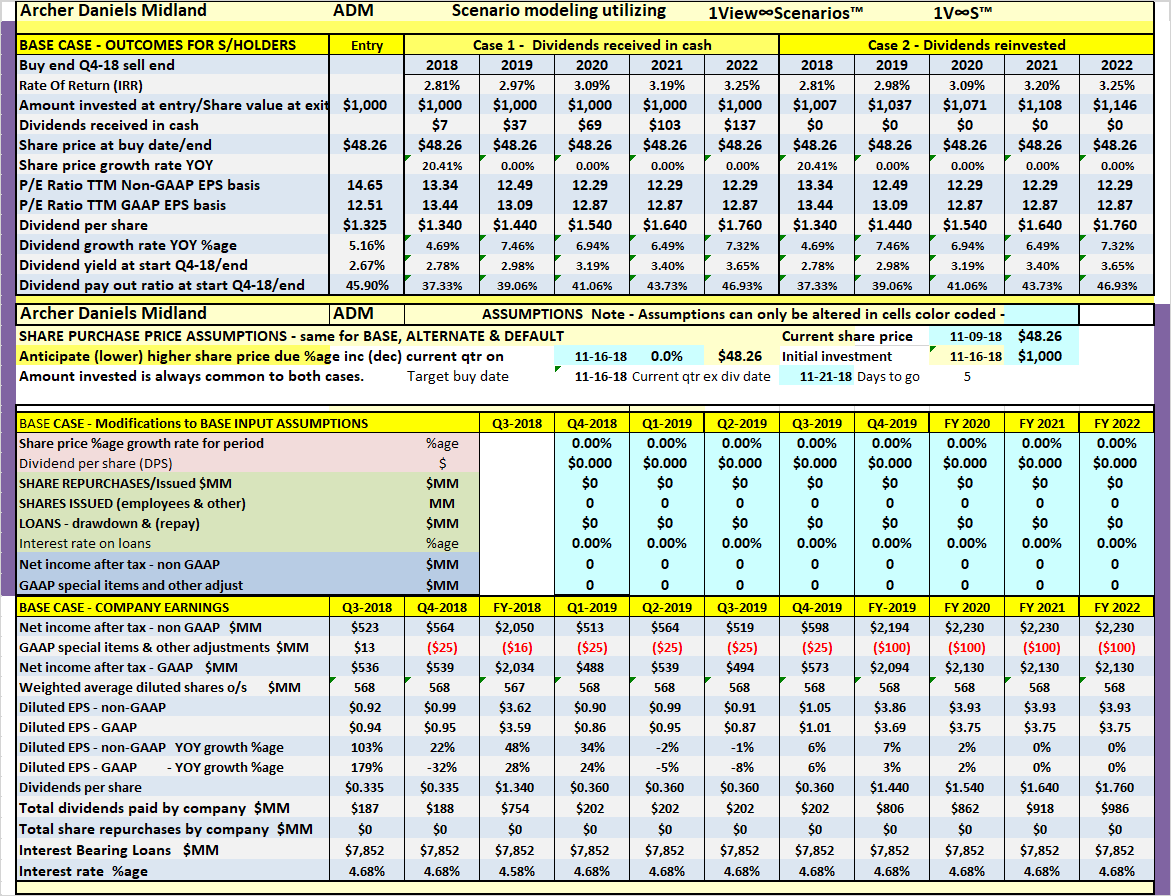

Interactive Dashboard Base Projections (similar in form and content to TABLE 3 and including rate of return projections)

This TABLE 4 dashboard is designed to allow us to create and modify a Base forecast by manipulating inputs and seeing the resulting effect on rate of return, share price, P/E ratio and other meaningful statistics. When we believe we have created a suitable Base scenario we can then move to Table 5 dashboard which allows us to interactively vary input and simultaneously see the effect on rate of return and other KPIs compared to the Base forecast.

TABLE 4 – Dashboard 1 Base Projection

Table 4 dashboard already has inputs for dividend increases and EPS based on analysts’ estimates. I have decided to make some adjustments before adopting as my Base projection. You will see I have input percentage increases for the input line item, “Share price %age growth rate for period”. The effect of these share price increases is to bring the non-GAAP P/E ratio up to 14.03 by the end of FY 2022. From TABLE 3 we can see between 2012 and 2018 the non-GAAP P/E ratio at year end ranged between 14.05 and 21.33. On this basis a target P/E ratio of 14.03 appears relatively conservative. Also note, in the absence of analysts’ forecasts for 2022, I have assumed 2022 EPS the same as for 2021. We can now go to our “Dashboard 2 Base And Alternative Projections” to conduct alternative scenario testing.

{kind=link}

TABLE 5 – Dashboard 2 Base And Alternative Projections

In Dashboard 2 above, I have input a number of changes in assumptions for an alternative scenario. The changes include:

- On or before May 31, 2019 an opportunity arises to purchase shares at $40.72, 5% below the current share price of $42.86;

- Yearly quarterly dividend increase adjusted upward by $0.005 to $0.02 for 2020 to 2022;

- Share repurchases of $450MM per year for 2019 to 2022;

- Average interest rate on borrowings increases by 1 percentage point at beginning of 2020.

- Non-GAAP and GAAP earnings increased by $50MM per year for 2021 and 2022 (see below).

- Non-GAAP P/E ratio increases to 15.0 by end of 2022.

The effect of all of the above is to increase the projected rate of return from ~10% per year for the base case, to ~15% per year for the alternative scenario. Of course, it is possible to construct an infinite number of scenarios by varying assumptions, and instantaneously seeing the impact on dividends, dividend yield, and total rate of return.

Re: Earnings, 2021 and 2022

From ADM’s Q3 2018 earnings call transcript:

Ray G. Young – Archer Daniels Midland Co.

So again, as Juan indicated, we talked about $1 billion run rate savings at the end of year two. So that means end of 2020. So that’s a run rate there. It’s going to build up over time. It’s not in a linear progression towards 2020. And also a part of it is going to be used to offset inflation. We do have inflation in our business, so part of the benefits will offset inflation and some market factors….And so I think how you should be thinking about it, it’s a gradual ramp-up, 2019, you recall we’re going to have benefits in 2019, but by 2020 you’ll get towards the run rate. It’s also important to note that it doesn’t stop at 2020. Readiness continues. And so while we’ve kind of indicated $1 billion end of 2020. When you get to 2021, 2022, there’s going to be also incremental benefits associated with Readiness.

On the basis of those statements, I have assumed, for Alternative scenario forecast, GAAP and non-GAAP net income after tax will grow by $50MM per year in each of 2021 and 2022.

To limit the amount of information on the dashboard, I have not included a “dividends reinvested” case. But I can assure all those DGI investors who follow Seeking Alpha, that the working model does provide results for the “dividends reinvested” case.

Outlook for Archer Daniels Midland

There are a lot of good initiatives in progress at ADM. It should definitely be worth while doing further scenario testing using the analysts’ “high” and ‘low” earnings estimates per TABLE 2 above to model further Alternative case scenarios to the consensus forecasts used for the Base case above. Those analysts’ estimates only extend out to 2021 and more detailed “own projections” for 2021 and 2022 are warranted. It would be interesting to flesh out the detail underlying the EPS forecasts with support from crowd-sourced subscribers with background in commodities trading and other specialist areas.

Apart from the current trade war effect on ethanol, it would be useful to look at the longer-term potential for this product. One thing for sure is this company has been around, and paying increased dividends for a very long time. That is unlikely to change. But for an investor in ADM shares, the single biggest determinant of likely return on investment is the entry price paid for shares. History shows there have been many opportunities for buying ADM shares at attractive prices in the past. But it is only by projecting the future we can get an idea of what current ADM share price level would represent a suitable entry point.

Different investors will have different ROR expectations. Use of a dashboard like those pictured above enables any investor to see whether ADM represents a buying opportunity for them at the current share price, and if not, at what share price it might be of interest. If there is concern at the effect of higher interest rates than those projected above, the effect can be easily seen with one or two simple inputs to the Base/Alternative scenario dashboard. Similarly, if the share price does go down, making share repurchases more attractive, this can be modeled to show the indicative impact on EPS and ROR.

If you wish to be notified of future articles, please click “Follow” next to my name at the top of this article.

Or become an Analysts’ Corner member. Share investing ideas with a like-minded group. Access 1View∞Scenarios™ dashboards to allow scenario testing for tickers of interest. You are welcome to register today for an absolutely no obligation 14-day free trial. Analysts’ Corner takes advantage of market sentiment and company fundamentals, to objectively target rates of return, rather than make purely qualitative assessments based on imperfect and inappropriate data.

Register now to join in the discussions on GE’s involvement in the hydrogen-electrical super highway.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stocks mentioned or to solicit transactions or clients. Past performance of the companies discussed may not continue and the companies may not achieve the earnings growth as predicted. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. I do not recommend that anyone act upon any investment information without first consulting an investment advisor and/or a tax advisor as to the suitability of such investments for their specific situation.